February 15, 2016

What to expect if oil storage capacity in Cushing fills to the brim

Commentary by Robert Balan, Chief Market Strategist

"In the second half, every tank and swimming pool in the world is going to fill and fundamentals are going to kick in… The market will start balancing in the second half of this year.” Robert W. Dudley, Group Chief Executive, British Petroleum, February 10, 2016

The Energy Information Administration (EIA) reported last week that crude oil stocks in Cushing, OK, had risen to 64.7 million barrels, 50% higher than levels seen a year ago. The EIA's latest survey of crude storage capacity on September 30, 2015, says that crude tank farm capacity in Cushing is 73 million, suggesting a spare capacity of just over 8 million barrels. Many observers and pundits suggest this may not accommodate a build as large as last year’s.

Moreover, EIA reported that petroleum product stocks have risen as well. Gasoline stocks increased by almost 25 million since the end of 2015 and are now at 255 million barrels. Distillate stocks have remained high due to lower usage on account of the warm weather in the Northern seaboard during early winter, which produced 21% fewer heating degree days than normal. The issue with high petroleum product stocks is that they depress refining margins, which as a consequence, create less financial incentive for refiners to operate at higher capacity. That theoretically would depress demand for crude oil. On the other hand, with better margins, crude demand could rebound, easing the ongoing oversupply issue.

But what is the implication of lack of spare capacity at Cushing? The facile answer is that it is negative for crude oil prices, as tight spare capacity will result in lower demand and in "backing out" crude imports, even as Iran starts to ramp up its oil exports. But not all analysts (including us) agree that this is what will happen. We believe that with prices already low, and in many cases, well below the threshold of operational profitability for many US oil producers, the optimal action will be to keep the oil in the ground. That is, capping the well. We believe that many shale oil producers, under prevailing conditions, could find this to be a reasonable solution to the problem of lack of storage. There is also no doubt that as the spare space continues to fill up, cost of storage will skyrocket, making this simple solution even more appealing. The speed at which US shale producers can respond to a firming in prices is legendary – so they can also respond just as fast to the lack of storage space. Shale producers can quickly go back on-stream once storage conditions or the oil price become more favorable. Shut-ins will also contribute to a recovery in prices, as output diminishes, lifting up market sentiment, which can lead to higher oil prices. It is a beneficial feedback loop.

It is also important to understand why tanks are topping out in Cushing at this juncture. Hark back to our basic premise that the shale oil revolution was facilitated (“greased”) by liquidity from the multiple Quantitative Easing (QE) program launched by the Federal Reserve. Commercial banks were flush with liquidity looking for home, and they found them in master limited partnerships and independent drilling firms intent on boosting oil and gas output quickly with fracking technology. So intense was the banks’ reach for yield that even as late as Q1 2015, when the oil price collapse was accelerating, the Financial Times reported that firms engaged in oil and gas exploration and development were able to raise more than $10 billion. That had provided the wherewithal for independent producers to continue drilling and fracking, even increasing production despite the sharp decline in oil prices.

The largesse from QE liquidity also enabled the construction of additional tanks which enlarged U.S. capacity to hold oil, which softened the already sharp collapse in oil prices. Why so? There is empirical evidence and industry lore which show that inventory increased as oil prices fell, and as the US Dollar strengthened (see first chart of the week below). The availability of new storage has made possible higher stock builds because it could be very profitable to purchase and hold oil under current low oil market prices and the US Dollar’s high purchasing power.

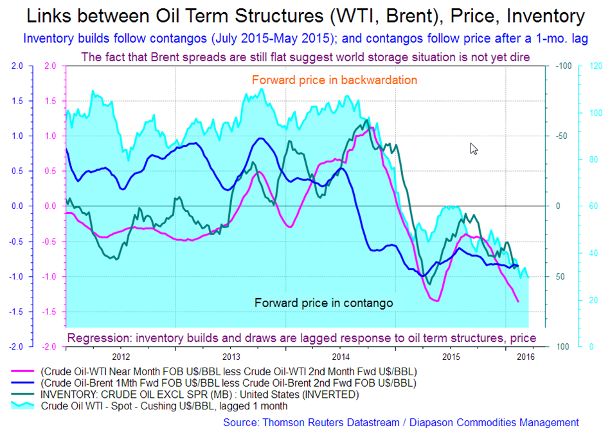

Investors can buy/import oil, store it, and sell contracts to deliver it at a higher price in six months or a year. Moreover, the near zero-interest regime enables financing with cheaply borrowed money, and return on these transactions can be substantial even after deducting loan and storage costs. It has been said that there is essentially very little, even no risk, associated with storing WTI crude in Cushing, OK, because the party holding the oil can deliver it under the futures contract and collect payment. However, the benign conditions that allow this money-minting strategy to prosper will, at some point, turn around: oil prices are starting to firm, the US Dollar is weakening, and the capacity market is tightening, driving storage costs higher. The still benign conditions are reflected in the current oil term structure – there is still a steep contango in the WTI one-two spread (see second chart of the week below). But it is a local WTI phenomenon – we do not see that steepness in the Brent’s one-two spread – which suggests that capacity utilization elsewhere in the world is not as dire as it is in Cushing. This brings us back to our basic argument that Cushing storage issues are more important for the WTI structure than for general oil pricing.

It is not also sure whether or not storage capacity in the US is filling up fast. Despite record stockpiles, the US still has probably 200 million barrels of space available, after inventories have been adjusted for pipeline fill and for crude in transit. The USGC alone is said to have perhaps 125 million barrels spare capacity left. Even assuming 20% of this available space is inaccessible because it is needed for blending and tank bottoms, it is likely that the Gulf Coast still has some 100 million barrels space left. Note that this available space may not be in Cushing, but these are indeed valid storage options, given the rising storage costs in the Cushing area. Exports could also be one low cost option in a cost curve of differentials. We do not doubt that if the Cushing situation turns gets worse, US exporters of oil will ratchet up their tempo.

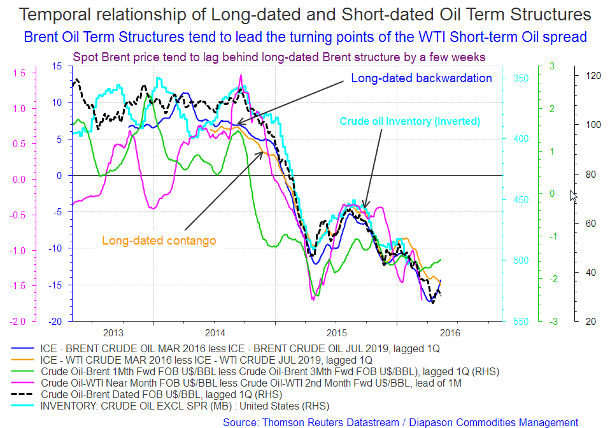

The global storage space condition is also still benign. As from early January, there may still be 500 million barrels of remaining capacity. Although excess crude supply beyond global demand has resulted in seasonally abnormal inventory builds, global crude stocks will not likely reach full capacity even if crude inventory levels continue to increase through 1H 2016. Improving global market balance may also do its part in alleviating the storage issue. By the end of 3Q 2016, the crude market should return to seasonally normal balances, with draws anticipated for 3Q 2016 and 4Q 2016, which should begin to lessen the pressure of high inventory levels globally. By that time, we may have already forgotten this buzz about topping out oil tanks in Cushing, in an energy world with firmer oil prices, and a WTI one-two spread that is making its transition from steep contango to slight backwardation. At that time, crude oil inventory should have peaked, responding to the earlier impact of higher oil price, and disappearance of the WTI contango (see third chart of the week below).

|

Main drivers this week:

|

Commodities and Economic Highlights

Commentary by Robert Balan, Chief Market Strategist and Sammer Khatlan, Oil Analyst

International Petroleum Week & Agency Reports: Oil market put in to perspective

Last week, London hosted its annual International Petroleum (IP) Week, giving market players from around the world the opportunity to network and debate the current state of the oil complex. We also had the key agencies – the IEA, OPEC and the EIA – release their respective monthly reports and forecasts which gave traders more food for thought as they navigate the uncertain waters of the oil markets.

This year has begun with a further price fall, below the psychological $30 per barrel level for crude, as OPEC maintained its ‘market share’ strategy, the US’ production remained comfortably above the 9 million b/d mark and Iran was welcomed back to the market. Feedback from various discussions and presentations on the market’s outlook from IP Week has followed a similar theme: bearish oil prices for 1H 2016 with a recovery of sorts expected to kick off in 2H 2016.

Irrespective of the price trend/direction, it is widely accepted that we can expect a range-bound market going forward and that before any ‘true’ rally can occur, the huge crude overhang will need to clear. The use of ‘true’ is important here: we recently wrote about the false hope that the OPEC/non-OPEC rumours gave prices several weeks ago before falling away as the key Gulf players, mainly Saudi Arabia, remained silent. As we have contended for some time, no sustained rally can occur until we start to see meaningful production declines in key areas of non-OPEC or OPEC cuts output. Last week, a new headline emerged: Venezuela proposed an OPEC, non-OPEC oil output ‘freeze’ during its producer tour – this is seen as an attempt to wrestle the global glut without cutting supply. Prices did rally on Friday but were still down on the week.

Volatility has hit a six-year high with significant positions being accumulated on both sides of the market. We feel this goes some way to explaining much of the current sentiment as market players are certainly undecided about the next steps to take. For those from the ‘glass half-full’ perspective, current price levels are unsustainable for all oil producers and market positioning is perilously short. Those ‘glass half-empty’ advocates will no doubt produce the recent agency monthly reports: IEA said that OECD commercial stocks built in December to 3.012 billion barrels, 350 million barrels above average, and will continue to grow into 2016 and 2017. It also reported that OPEC crude output rose again in January, standing nearly 1.7million b/d higher YoY. The EIA reported YoY growth in total oil supplies outside of OPEC (+1.4 million b/d in 2015) whilst OPEC reported non-OPEC oil supply for 2015 was revised up to +1.32 million b/d YoY, due to OECD, Developing Countries and the FSU.

The price action last week confirms that market bears are still very much in the game. The momentum-trading nature of CTAs means that futures prices can be pushed down further from current levels; anecdotal feedback has informed us that whilst many active paper traders and physical crude traders have priced in the current oversupply, they will not discount the possibility of algorithmic programmes driving futures prices down even further given that the CTAs can be leveraged anything from 5 to 20 times, giving them the volumes to bully out any nascent bullish positioning.

We continue to believe that Gulf-OPEC will maintain its stance and not cut output. Once again Saudi did not respond to the latest ‘freeze’ headline and comments from the UAE (the likely cause of Thursday’s rally) did not offer anything new. However, current market positioning is such that any headline can trigger a significant round of short covering, as we have seen.

We have contended that the medium to long term fundamentals for oil are critical and market players are starting to come around to this reality, as observed in IP Week. Billions of dollars of future investment in global exploration and production have been erased: for example, less than two months into the year, the top US shale names have already cut their budgets for a second time for 2016. Wood Mackenzie recently estimated that the world will not see 2.9 million b/d of future production as a result of the global upstream cuts.

Involuntary output cuts will also begin to filter through. FSU production is looking increasingly vulnerable with Azerbaijan having an emergency meeting with the IMF to secure a possible $4bn bailout loan and Russia delaying some 30 licences for pipelines and fields. Asian and Latin American producers have also mentioned output cuts and US independents have guided towards falling production this year. Indeed, the aforementioned agencies have all forecasted US supply to drop YoY in 2016: OPEC by -0.4mmbd and the IEA and EIA by -0.5mmbd. The wider consensus is that non-OPEC will see output contraction this year.

The latest OPEC, non-OPEC headline may be nothing more than just speculation but the market is clearly getting anxious about the increasing level of chatter from high level officials in key oil producing states. Any positive statement or action from the Gulf or if non-OPEC starts to see material output declines, market shorts will be spooked into desperate action.

Tin enjoys a large recovery as output cuts were announced, LME stocks fall

Alongside the base (and precious) metals complex, tin is enjoying a recovery following supply cut announcements. Tin prices have risen since falling to a low of $13,085 per ton in the middle of January. The metal is up 18.8% from its 2016 low. The current recovery has been driven by several factors that have driven the prices of other base metals as well – supply cuts were announced and China started to buy at the end of 2015. Those announcements did not get an immediate response from the price action, as the period was marked by a resurgence of a risk-off environment. Fears of a hard landing in China resurfaced, and investors responded by trimming exposure to risk assets, including base metals. After that, the US Dollar weakened significantly, prompting investors to reconsider investments in base metals, including tin.

Tin supply tightened considerably after nine large Chinese smelters – YTC, China Tin, Chengfeng, Zili, Kaimeng, Yunxin, Jinye, Nanshan and Weitai – in January agreed to cut production by 17,000 tons or 12% in 2016 to check the steep decline in the metal's price. These Chinese companies produced 140,000 tons in 2015, which comprises almost 80% of Chinese tin output and 40% of global output. The group also requested Chinese authorities to consider a strategic stockpile program. The point was that state strategic stockpiling would be the best option for producers and the country. Alternatively, they also proposed that if private stockpiling is preferred, the government should subsidize interest payments to compensate the cost of carrying inventory. The Chinese government had no explicit response to the petition, but the market seems to be optimistic about the implementation of such a stockpile program. Spot prices started to rise not long after, suggesting that the petition maybe under serious consideration by the government.

Moreover, Indonesian refined tin exports continue to be constrained. Indonesia exported 5,805 tons of tin in December 2015, down 44% from the year before. In 2015, Indonesian exports totalled 70,150 tons, down from 75,925 tons from 2014 and the 88,443 tons exported in 2013. Exports of refined tin are expected to decline further in 2016, in large part due to tightened regulations and stricter "clear and clean" (C&C) certification, and due to adverse market conditions. The tightening tin market balance is being highlighted by the continued drawdown of LME stocks. After declining 5,970 tons (49%) in 2015, stocks fell another 1,520 tons or 25% so far this year to 4,620 tons. Significantly, the cash-to-three-month spread has remained in backwardation for most of 2016, which suggests building pressure from short-covering. Interestingly, latest LME statistics corroborate that a short-covering is taking place. Investors added to their net long positions by 485 lots to 1,658 between January 22 and January 29, and also short-covered 68 lots and posted long accumulation of 417 lots. The short-side speculative positioning has clearly overstretched, with liquidation of 1,680 lots or 50% of their long positions between October 2015 and January 2016. If tin price move higher further, we should see a strong impetus from short-covering.

The demand side of the tin supply-demand balance however poses some downside risks. There was fairly weak demand in 2015. Growth in semiconductor shipments (indicator of tin demand in solder alloys, which represents about 50% of global use) slowed last year. According to the Worldwide Semiconductor Trade Statistics (WSTS), the worldwide semiconductor market expanded at only 0.2% last year and is expected to grow at 1.4% in 2016, and 3.1% in 2017. The tinplate sector, representing 20% of global use, also saw demand as sluggish because tin packaging faces increasing competition from aluminium and plastic packaging. The rally in tin prices will likely continue until late Q1 2016, reflecting recent supply cut announcements, and the low level of LME stocks. But if the broad improvement in sentiment across the metals continues, then that could induce a wave of short-covering. We expect a better tone to tin and other base metal prices by H2 2106 as the China situation clears up, for the better.

Charts of the week: Oil inventory builds accelerated as price fell and USD TWI strengthened; links between oil term structures, price and inventory; Brent term structures leads turning point of WTI short-term spread

|

|

|

|

|

|