February 1, 2016

2016 outlook for base metals: prices should pick up in H2 2016 as supply deficits grow

Commentary by Robert Balan, Chief Market Strategist

"I believe that the testing of the dip of copper price beneath US$2.00 per pound during the past few days and recovery of copper back to $US$2.05 may signal the bottom for this cycle; although this seems to be a positive, we will need to wait for copper to break out above a range of $2.00 to $2.20 per pound.” Dr. Harlan Meade, Copper North President and CEO, January 26, 2016

Global resource producers have suffered major setbacks in the past few years in the form of sharply lower base metals prices and collapsing equity prices. Those developments can be attributed to several factors: perception of slowing Chinese growth, a surging US Dollar, and a massive crash in oil prices. China's faltering growth was the main driver in the collapse of resource materials. China is the world's biggest consumer of commodities (40% of global copper demand comes from China, for instance). As a result, the global miners' and producers' equity prices have been suffering major declines since 2013.

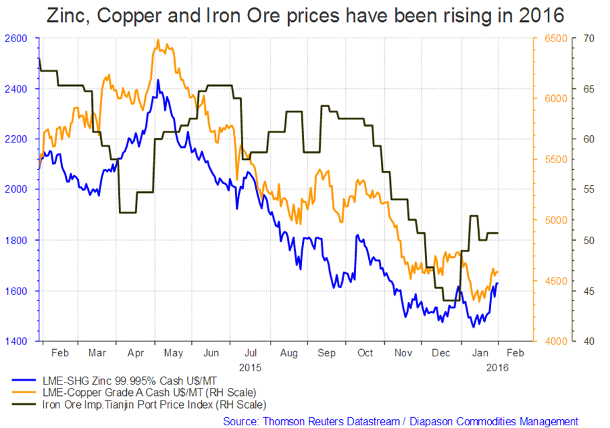

Metal miners and producers have been under pressure to act, and they have taken several steps to alleviate the situation. They have (1) slashed exploration budgets, and capital spending, (2) closed mines, laid-off thousands of workers and cut output, (3) substantially reduced their outstanding debts, (4) increased efficiencies in production by focusing on profitable operations, and finally, (5) cut or suspended dividend payments. For instance, Freeport-McMoRan suspended its dividend last December; Glencore also announced steeper cuts to its debt and capital spending plans and issued upbeat guidance last December. These steps had significant positive impact on those major producers share prices, as well as boosted the shares of Freeport-McMoRan, Rio Tinto, BHP Billiton, and other miners. But the impact on the prices of base metals has been mixed so far. But we believe that the situation should change by H2 2016. We believe that the demand-side will remain stable and in fact may even improve by late H2, and on the supply-side, we could see the initial stages of a "supply crunch" by H2 2016. Three metal commodities may present the best case on the supply side this year: zinc, copper and iron. The inclusion of iron (or technically, iron ore) in this list is crucial as it has been one of the worst performing resource commodity for the past two years. All of these metals have been rising in 2016 (see the first chart of the week below).

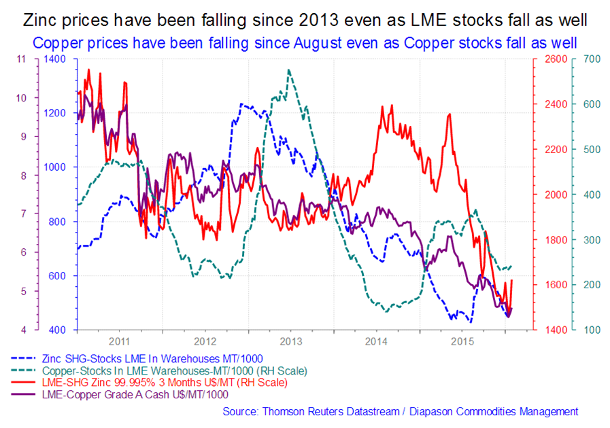

Global zinc production losses were significant in 2015. For example, in China, production has been down by 60-70%, mainly due to low prices, environmental issues and the government's decision to delay the renewal of licenses for smaller mines in its crackdown on pollution. China's zinc demand has significantly risen, also partly due the expected protracted devaluation of the CNY, moving importers to pre-empt the domestic currency's weakness. The country's zinc imports rose to highs not seen since May 2009, and were up by over 400% during December 2015 alone, mostly on concerns about tightening supplies in 2016. Globally, zinc production has been declining due to issues with several blockbuster mines such as Australia's Century, which has reached its end-of-life cycle with little prospects of new production in the pipeline. A Reuters survey late last year shows that analysts believe Zinc will have an estimated global deficit of 53,000 tons in 2016 and 275,000 in 2016. Copper shipments in December reached their highest level since at least 2008.

Another sharp commodity supply crunch in 2016 may come from copper. Some experts recently issued warnings about the looming production shortage in the commodity. "The reduction in supply could cause prices to spike in 2016", said the International Copper Study Group which lowered copper production forecasts in October 2015. The Group said that there will be 130,000 million tons deficit in 2016. "We expect the copper market will record a deficit before the end of 2016", analysts at Intesa Sanpaolo, also stated in October 2015. In December, Wood Mckenzie said that 2016 will be the year when production cuts by the major producers will start to be felt, while demand remains strong. In the longer term, Wood Mackenzie predicts a deficit of 10 million tons of copper by 2028 (see second chart of the week below).

The case for supply shortages in iron ore is not as compelling as for the two other commodities discussed above in 2016. Nonetheless, there are signs that production is already moderating as higher cost producers are being squeezed out of the market. Excess supply of iron ore is currently being absorbed by strong demand coming from outside China, moving some analysts to negate previous reports of an oversupply in 2016. Iron ore imports in 2015 increased by 17% from the prior year and soared to an all-time high. Rio Tinto reported that demand for iron ore is expected to remain strong in 2016 with primary growth coming from India, the Middle East and Southeast Asia.

Widespread monetary easing should make another appearance this year, courtesy of the ECB, Japan, and likely, China. The intention is to battle disinflation and to lift consumer spending. Metal prices rose after the ECB's Mario Draghi hinted at new monetary stimulus. Japan also went the way of negative interest rates boosting market sentiments. Some banks have discarded their bearish bias on base metals. For instance, BNP Paribas, in October last year, advised against taking aggressively negative positions versus base metals, saying that the bank expects growth in world base metals demand to pick up by 3% in 2016 relative to 2015 levels. Indeed, the outlook for base metals are picking up. The only factor that weighs on the market is the perception that Chinese growth will continue to fall, impacting global growth which could impact base metal demand. We believe that this perception is unfounded, and that Chinese activity should improve later in H2 2016. The US Dollar could also be weaker in H2 2016, as global growth continues to pick up. That should act as further boost for base metal prices, which we expect to outperform the rest of the commodity sector.

|

Main drivers this week:

|

Commodities and Economic Highlights

Commentary by Robert Balan, Chief Market Strategist and Sammer Khatlan, Oil Analyst

Sanction relief: The short-term reality of Iran’s return to the market

Whilst the uncertainty of sanctions has been removed (at least in the short term), the timing and size of additional Iranian supply to the oil market remains unknown; this has stimulated much debate and analysis. We believe that the return of Iran has been priced in for some time now and arguably, we saw the immediate impact on oil prices in July 2015 as Brent fell 4% following the announcement that the world powers and Tehran had reached a deal.

Additional Iranian supply will come from two sources: floating storage and new production. Let us begin the former: it is estimated that 30-40 million barrels has been stored offshore in VLCCs. However, this oil is mostly condensate and fuel oil. Condensate is a by-product of natural gas production and is often used to blend with heavier oils to process into fuels. Outside of Asia, refineries have a limited appetite for condensate as the bulk of capacity is geared towards heavier crude grades, needing simple plants called ‘splitters’ that can turn pure condensate into naphtha, an important petrochemical feedstock. Iran has traditionally enjoyed strong presence in the Asian market for condensate yet competition from Saudi Arabia, Qatar and Australia has reduced this foothold somewhat. At the same time, Dragon Aromatics, Iran’s biggest buyer of the ultra light oil (2 million barrels out of the 9 million produced) suffered a fire at its Fijian plant and has been shut down since April 2015. No restart date has been announced at the time of writing.

Offshore storage of crude is said to be less than 10 million barrels, according to officials. China, India, Japan, South Korea and Taiwan have been able buy Iranian oil at reduced volumes under a waiver from US sanctions, capped collectively at 1mmbd. However, the crippling oil and financial sanctions imposed by the EU and US have seriously hampered Iran’s presence in the region. China is the key market and Tehran has had to watch on as Saudi Arabia and Iraq consolidated and built upon their footholds. The space left by Iran has also been filled by Russia, who have more than doubled exports to China since 2011.

Iran’s forecast output growth comes mainly from pre-existing capacity that has been shut-in and newly developed fields. Rhetoric has softened since the oil minister’s claim of production growth of 0.5mmbd “within a week” and by 1mmbd within six months as Tehran will seek to avoid adding to the current oversupply – indeed the continued collapse of international oil prices will have spooked the ministry even further. Iran’s upstream has suffered from decades of under-investment and sanctions prevented any western technical or financial intervention. Russia and China were brought in to develop projects, including several new fields but these relations have been strained and in some cases, have broken down completely. Existing fields, namely Iran’s largest and most mature reserves, were deliberately ramped down when sanctions came into effect; this accelerated decline rates. Several new fields such as those in South Pars, North Azadegan and Azar can provide fresh supply but these projects have been delayed frequently and there are no guarantees that they will come online as planned or even hit expected capacity. We believe that any production from these new fields will not offset the losses from the existing fields owing to decline rates.

The initial impact from post-sanctions will initially come from storage and then from domestic production after stockpiles are cleared via exports. Iranian output suffers from significant technical constraints as the lack of foreign investment and insufficient financing has slowed down development. Existing fields, particularly the mature fields that started pumping some 70 years ago (including the Ahwaz-Asmari, Marun, and Gachsaran fields) cannot handle any immediate, aggressive ramp ups in activity and have been impacted by decline rates – the expertise and investment from Western companies is crucial at this juncture.

Western companies will tread carefully before entering the Iranian market as prominent risks remain, for example: heavily indebted local banks, corruption, an archaic legal system and an obstinate labour market. In an already well-supplied market, Iran will need to offer favourable terms to entice and secure buyers; however the reality of oil prices below $30/bbl means that offering ‘sweet’ terms, under current market conditions, will only secure reduced revenues, limiting the economic benefits from increasing export volumes. Considering all the above, we believe Iran will effectively add between 0.3 to 0.4mmbd of supply to the market in the short-term, taking into consideration some 0.1-0.15mmbd of lost capacity through decline rates. Long-term, upstream investment, both financial and technical, can transform Iran’s fortunes however, the dynamics of the oil market could be in a very different place by then.

El Niño hits its peak soon; welcome to La Niña

El Niño is about to peak in a few weeks, and the event's more devastating sister, La Niña, may make its appearance not long thereafter. La Niña essentially poses the opposite effects of El Niño. It is the below normal cooling of sea surface temperatures in the eastern tropical Pacific Ocean. La Niña usually follows an El Niño event, but not always. La Niña events, like El Niño events, vary with each event.

Like El Niño, La Niña has predictable effects on the weather of the US Southeast. In a La Niña winter, the Southeast tends to be warm and drier than usual as the subtropical jet is pushed away from the region. Since winter is the recharge period for soil moisture across most of the US Southeast, La Niña may mean dry planting conditions in spring and a need for increased irrigation to get germination going. La Niña summers are also periods with high tropical storm activity, leading to potentially wetter conditions later in the growing season and harvest if the storms come to the region.

The question is this: what will La Niña bring to the agriculture sector? How are its effects different from El Niño? Which commodities will be impacted by La Niña? While El Niño and its impact might be better known, prices for crops such as soy, corn and wheat can move around 50% more during a La Niña event, based on a measure of the volatility of prices. We also get some answers from the transition of El Niño to La Niña during the events of 1997-1998. We are assuming of course that La Niña will follow El Niño, which is not a sure event. But nine manifestations of El Niño weather phenomenon were recorded starting in 1980 and not counting the current manifestation this year – and six of them were replaced by La Niña. If we consider the earlier events, the cadence makes it likely that a La Niña should occur at this time. This year's El Niño should be replaced by La Niña with a probability which we calculate at 70%. La Niña appears between 8 months to 12 months after El Niño peaks out.

If El Niño morphs into La Niña later in the year, the corn and soybean crop may be the most impacted by the change, based on what we have seen during previous events. For the US, La Niña potentially means dry weather in the south of the country, specifically within the Corn Belt. A La Niña's impact on the US corn production can be statistically assessed based on historical data. The data shows a decline in US corn yield by an average of 20% from trend, in four out of the six cases of La Niña manifestation. In the other two cases, there were no corn yield decreases below the trend, but there was no substantial growth either.

La Niña events are also associated with rainier-than-normal conditions are over south-eastern Africa and northern Brazil. Drier-than-normal conditions are however observed along the west coast of tropical South America, the Gulf Coast of the United States, and the pampas region of southern South America. The La Niña events also causes droughts in the south region of Brazil which are, basically, very harmful to the soybean crop in the region. For example, the 1988/1989 La Niña event was intense, the drought occurred mainly during the winter months. Unlike El Niño, which usually lasts no more than a year, La Niña events may last between one and three years – and that is what these events more harmful than El Niño. The likelihood that the current El Niño peaks soon and turns into a potentially strong La Niña by late 2016 or early 2017 is something that participants in agricultural markets should track closely. It may have a bigger impact on agriculture products than El Niño did.

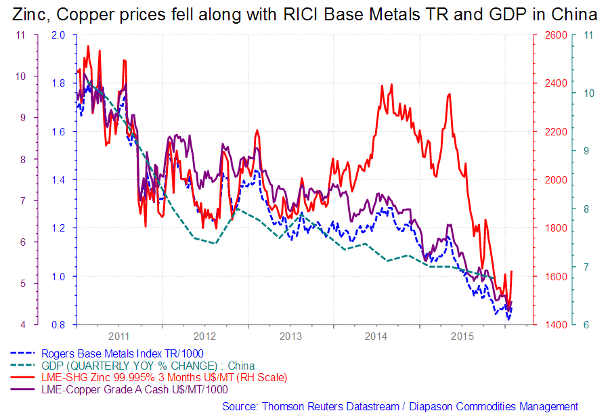

Charts of the week: Zinc, copper and iron ore prices have been rising in 2016; Zinc prices have been falling since 2013 even as inventories fell; Zinc and copper fell alongside RICI base metals and China GDP

|

|

|

|

|

|